Buybacks

Not all buybacks are created equal. But the good ones do incredible things.

“My suggestion: Before even discussing repurchases, a CEO and his or her Board should stand, join hands and in unison declare, ‘What is smart at one price is stupid at another’.” — 2016 Berkshire Hathaway letter.

Not all buybacks are created equal. But the good ones do incredible things.

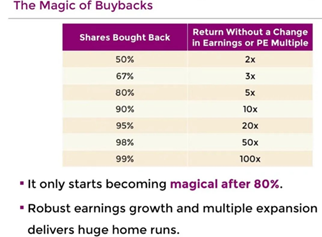

Mohnish Pabrai has a good slide on the magic of the math and how they can act a spring coil to share prices.

To buy back 80% of shares you need a very stable business that can keep feeding you cash for more than a decade

As a shareholder, management can give us three types of buybacks as a present.

1. The flowers buyback

We all love receiving flowers. They smell nice, look pretty, but unfortunately they don’t last very long.

In this first type of buyback, management has no opinion or conviction on the valuation of their shares. This means the buyback is generally small, insignificant and sometimes purely cosmetic in an attempt to support the share price with a vote of confidence from management.

Other times it could be purely to offset option and share based compensation dilution, e.g. “Given the macro environment and our strong free cash flow generation, we believe that using a portion of our free cash flow to manage dilution is a strategic use of capital”, ServiceNow CFO May 2023.

While admirable, its not all that strategic if you’re buying at silly prices.

2. The $20 Kris Kringle buyback

It happens once a year, maybe. It’s a gift, it might be fun, but you’ll probably throw it out in 2-weeks. They rarely have any value.

Again, management have no opinion on the valuation of their shares, but this time they are simply returning money to shareholders via repurchases as opposed to a dividend. It is more common in the US where there are greater tax advantages, as opposed to Australia which has franked dividends.

However, that doesn’t stop Aussie companies buying back shares willy nilly when they have excess cash. For a recent example, lets look at National Australia Bank (NAB).

In the panic of COVID in May 2020, the bank raised $4.25bn from issuing 300mil new shares at $14.15 per share. This was a 10% dilution.

Just over a year later, in July 2021, the bank started a $5bn buyback, retiring 172mil shares across nearly 2-years of on-market buying. The lowest price it paid was $25.44, and the highest price it paid was $32.14.

NAB effectively sold low and bought high. It’s hard to create shareholder value employing this strategy.

In this second bucket of buyback vs. dividend, it is also worth cross checking what management are incentivised to do.

“The further $2.5 billion on-market buy-back announced today supports our ambition to reduce share count and increase sustainable ROE (return on equity) benefits for our shareholders.” — NAB CEO Ross McEwan, March 2022.

Have a guess what the first financial metric is that determines Ross’ long term incentive bonus payout. ROE.

And other than increasing profits, what increases ROE? Buying back shares, as it reduces the denominator of this ratio (equity).

3. The valuable buyback

It might have been your 21st present, a special wedding gift, or you know those people that are really good at gift giving? These presents have value.

This is the type of buyback program where managements have correctly identified a mispricing of their company and by retiring shares, they are going to leverage returns to the long-term shareholder. This is a very rare skill.

As Ross showed us, managers, much like investors, struggle to follow the adage of “buy low, sell high”.

“Overconfidence can lead executives to buy back shares even at the peak share price — and a bias for caution can restrain them from buying shares when prices are lowest. The result is that companies seldom consistently pick the right time to buy back their shares at advantageous prices. Indeed, for the years 2004 through 2010, our analysis finds that a majority of companies repurchased shares when they and the market were both doing well — and were reluctant to repurchase shares when prices were low relative to their intrinsic valuations. Few stopped repurchases even as the market peaked in 2007. And when the market bottomed in 2009, few companies were buying back shares.” — McKinsey

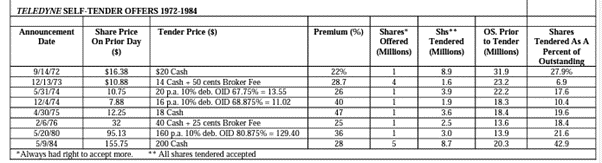

Few have been successful, so lets look at the king of buybacks, Henry Singleton. He generated an incredible 20.4% p.a. of shareholder returns across his nearly 30-year tenure of the conglomerate Teledyne.

Prior to the 1990s, buybacks were seen as a sign of weakness. It indicated that your business lacked investment opportunities internally, and the conventional thinking was why on earth would you want to shrink your business? But Henry Singleton ignored Wall Street’s opinions.

In 1972, with a growing cash balance and Teledyne’s share price collapsing (in line with the market) from $40 to $8, Singleton saw an opportunity where no one else did. He proposed to the board that they could earn a better return buying their shares at these levels than doing anything else. So, between 1972 and 1984, in eight separate tender offers, he bought back an astonishing 90% of outstanding shares.

These buybacks were super aggressive and timed with low stock prices. As opposed to sipping from a straw for two-years, buying back shares gradually on-market, Singleton took to buybacks like a suction hose.

What’s even more incredible is that in the decade prior, Singleton grew shares outstanding by 14x as he rapidly acquired 130 companies. His ability to flip from this mentality and understand the value of his business was incredible.

“Great investors (and capital allocators) must be able to both sell high and buy low; the average price to earnings ratio for Teledyne’s stock issuances was over 25x. In contrast, the average multiple for his repurchases was under 8x.” — From the book Outsiders.

In general, we love our companies to be buying back their stock. It increases our ownership interest, and as we repeatedly say, we are focused on the growth of free cash flow per share.

But buybacks are just one tool in a manager’s capital allocation toolbox. They can be a significant source of value creation, but they can also destroy shareholder value if made at silly prices.